The short but busy week closed on the downside with S&P 500 ending the week down 0.55%. Economic reports were mixed but most of them indicated a slowdown.

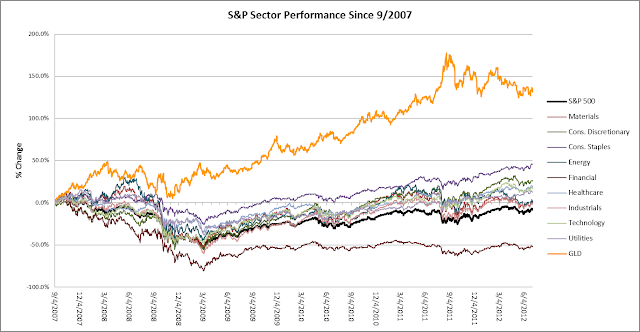

Sector performance update for this week is provided below.

- Manufacturing ISM for June came in well below expectations and lower than 50.0, which meant it is contracting.

- Construction spending for May was better than expected and the April figure was revised higher.

- May factory orders also came in better than expected, but was partially offset by the downward revision of the prior month.

- Initial claims were lower than consensus, but remained above 350K. The upward revision momentum of the prior week was broken as the prior week was revised down for the first time this year. Continuing claims continued to increase.

- The significantly better than expected June ADP figure certainly upped everyone's hopes that the official June employment report will be a good one. Economists increased their projections which led to a +5K adjustment in the NFP consensus to 100K.

- June services ISM was disappointing but unlike manufacturing, it remained above 50.0.

- Lastly, the June official employment report disappointed most economists as net change in NFP of 80K was significantly below the 100K estimates. Our estimate called for a 74K increase. There were a couple of bright spots in the report which we mentioned in our last post.

Sector performance update for this week is provided below.

No comments:

Post a Comment